The Cheapest Option Is Often the Most Expensive

What Beaverton Property Owners Get Wrong About Turnover Costs

One of the most common mistakes rental property owners make is evaluating turnover decisions based only on the immediate invoice instead of the long-term financial outcome.

On paper, saving money during a turnover can feel like the conservative decision. Spend less today, protect cash flow, move on.

But in property management, the cheapest short-term option is often the most expensive long-term option.

Recently, we managed a turnover for a single-family home in a strong Beaverton-area neighborhood. The property itself showed well from the outside. Good curb appeal, solid location, desirable layout. The home was roughly 15 years old and had been used as a rental for quite some time before coming under our management.

Unfortunately, the outgoing residents had been fairly rough on the interior.

The walls showed significant wear. There were visible touch-up differences throughout the home, inconsistent paint sheen, scuffing, patched areas, and general cosmetic fatigue that had accumulated over years of rental use.

Our recommendation was straightforward:

perform a full repaint before marketing the property.

The owner understandably hesitated at the cost. Instead of approving the recommended roughly $3,500 repaint proposal, the owner pushed back and asked us to explore the absolute minimum necessary to prepare the home for market.

When we sent the painter back out to reevaluate the property, the conversation was essentially:

“What is the bare minimum needed to make this home rentable while still allowing you to stand behind the work?”

The answer came back at approximately $850.

Importantly, this was not presented as the ideal solution.

It was presented as the minimum acceptable solution.

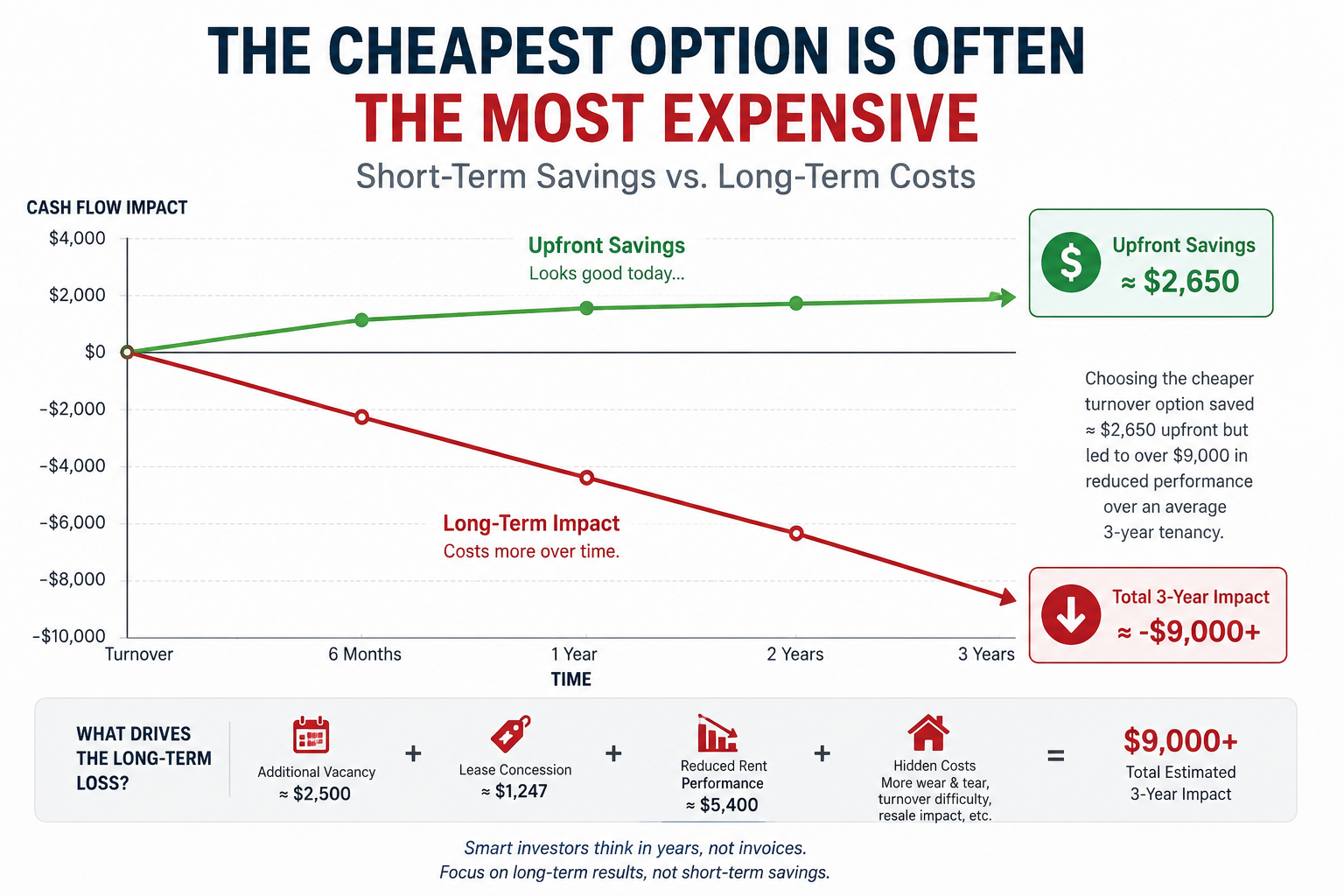

On paper, that appeared to save approximately $2,650 upfront.

Unfortunately, the long-term financial results likely moved in the opposite direction.

The Problem With Evaluating Turnovers One Invoice at a Time

Many owners unintentionally evaluate turnover decisions in isolation.

“How much does the paint cost?”

“How much does the flooring cost?”

“How much does the cleaning cost?”

But experienced real estate investors eventually learn that turnover expenses cannot be evaluated independently from leasing performance.

The real question is not:

“What costs the least today?”

The real question is:

“What decision produces the strongest overall financial result for the property?”

Those are two completely different ways of thinking.

In this particular case, the home ultimately sat vacant for more than 30 additional days beyond what we would typically expect for a home in that neighborhood and price range.

At approximately $2,500 per month in market rent, that additional vacancy alone represented roughly $2,500 in lost income.

But that was only the beginning.

The property also ultimately rented below the original target pricing by approximately $150 per month.

That reduction may not sound dramatic initially, but over the course of a single lease term, that equals roughly another $1,800 in lost annual revenue.

Additionally, a concession equivalent to roughly half a month free rent was eventually offered to secure a tenant.

That concession represented another approximate $1,247 reduction in income.

Suddenly, the “savings” look very different.

Approximate First-Year Financial Impact

Upfront savings from avoiding full repaint: ≈ $2,650

Additional vacancy loss: ≈ $2,500

Lease concession: ≈ $1,247

Reduced annual rent performance: ≈ $1,800

Estimated first-year financial impact:

approximately $5,500+ in losses to avoid spending an additional $2,650 upfront.

And importantly, this is not theoretical math pulled from a textbook. This is the type of real-world situation property managers encounter regularly.

The Compounding Effect Most Owners Miss

And the most important part is that these impacts rarely exist for only a single lease cycle.

For a single-family rental home in a neighborhood like this, an average tenancy of roughly three years would not be unusual.

That means the reduced rental performance alone may continue compounding for years.

Approximate Three-Year Financial Impact

Additional vacancy loss: ≈ $2,500

Lease concession: ≈ $1,247

Reduced rent performance over three years: ≈ $5,400

Estimated three-year impact:

approximately $9,000+ in reduced performance to avoid spending an additional $2,650 upfront.

And that still does not account for:

increased future turnover difficulty,

cumulative cosmetic fatigue,

weaker applicant pools,

accelerated wear and tear,

or reduced resale flexibility.

A proper repaint often lasts years when completed correctly.

Ceilings may last close to a decade.

Doors and trim can often survive multiple turnovers with only touch-up work.

Well-prepared wall surfaces become significantly easier to maintain over time.

By contrast, partial cosmetic solutions frequently create long-term inconsistency.

Once mismatched touch-ups, sheen differences, patchwork repairs, and aging paint layers accumulate, future touch-up work becomes increasingly difficult. At some point, the property begins carrying a persistent “tired” appearance that follows it from turnover to turnover.

And because occupied residents generally do not want painters moving throughout the home, owners often lose the opportunity to fully correct those cosmetic issues later without creating significant disruption.

In many cases, the property effectively becomes locked into mediocrity until a future vacancy finally creates another opportunity to reset the condition properly.

Unfortunately, that can take years.

Cosmetic Condition Changes the Applicant Pool

One of the less discussed realities of rental housing is that property condition directly affects applicant quality.

Residents absolutely notice cosmetic condition during showings.

Fresh paint communicates:

cleanliness,

care,

maintenance,

professionalism,

and pride of ownership.

Tired paint communicates the opposite.

Unlike owner-occupied homes, rental properties are rarely professionally staged during showings.

Prospective residents are not evaluating furniture, decorations, or interior design choices.

What they primarily see is:

flooring,

walls,

paint condition,

lighting,

cleanliness,

and fixtures.

There are very few distractions.

That means cosmetic condition often carries significantly more visual weight during a rental showing than many owners realize.

When a home shows visible cosmetic fatigue, it can unintentionally filter out some of the strongest applicants. Residents who value cleanliness, maintenance, and long-term care of a home are often the same residents who notice cosmetic condition during tours.

Those residents frequently have choices.

If another comparable home nearby feels cleaner, fresher, brighter, and better maintained, they often choose the competing property.

As a result, deferred cosmetic work can gradually shift the applicant pool toward residents who are more tolerant of deferred maintenance and lower overall property standards.

That can create additional downstream costs that are difficult to quantify:

increased wear and tear,

higher turnover costs,

more resident complaints,

lower resident satisfaction,

and greater difficulty maintaining the property long term.

Cosmetic Condition Impacts More Than Rent

One of the biggest misconceptions in rental property ownership is that cosmetic condition only affects rent amount.

In reality, it affects:

marketing performance,

days on market,

photography quality,

applicant perception,

negotiation leverage,

concession pressure,

future turnover ease,

and even resale flexibility.

Life changes.

Owners relocate.

Financial situations shift.

Properties get refinanced.

Investment strategies evolve.

Unexpected sales happen.

If an owner suddenly needs or wants to sell a property during an active tenancy, the cosmetic condition inside the home may be largely locked in until that resident eventually vacates.

That means decisions made during one turnover can impact not only leasing performance, but potentially future resale value and marketability as well.

Sometimes the “Expensive” Recommendation Is Actually the Conservative One

This is one of the biggest mindset shifts experienced investors eventually make.

The goal is not minimizing every invoice.

The goal is maximizing long-term asset performance.

Sometimes that absolutely means controlling costs aggressively.

But other times, the more expensive recommendation is actually the more conservative financial decision because it:

reduces vacancy,

preserves pricing power,

improves applicant quality,

protects the condition of the asset,

simplifies future turnovers,

and creates stronger long-term financial outcomes.

Professional real estate investors do not simply ask:

“What costs the least today?”

They ask:

“What decision produces the strongest long-term result over the life of the investment?”

That distinction matters enormously in property management.

And very often, it is the difference between protecting cash flow and slowly eroding it over time.