Why Every Rental Property Owner Needs Reserves

One of the most common mistakes I see rental property owners make is viewing the difference between the rent collected and the mortgage payment as profit.

While cash flow is important, rental property ownership includes future expenses that may not occur for years but are nonetheless part of the cost of owning the asset. Roofs wear out. Furnaces fail. Water heaters need replacement. Tenants eventually move out. Flooring, paint, appliances, and other components all have finite service lives.

Successful owners understand that rental property should be evaluated over years and decades rather than months. A property may operate with very few significant expenses for a long period of time and then require substantial investment within a relatively short window.

For that reason, every rental property owner should maintain reserves.

What Are Rental Property Reserves?

When I refer to reserves, I am not referring to the maintenance reserve balance that many property managers require owners to keep on hand for vendor dispatches and invoice payments.

I am referring to the funds an owner sets aside to operate a rental property as a long-term investment.

Reserves generally serve three purposes:

Funding future capital expenditures.

Covering vacancy and turnover costs.

Providing a cushion for unexpected maintenance and repairs.

Many real estate investors use a simple rule of thumb of allocating approximately:

2.5% of rents toward maintenance

2.5% of rents toward vacancy and turnover

2.5% of rents toward capital expenditures

This results in a reserve contribution target of approximately 7.5% of gross rents.

While that approach provides a useful starting point, it assumes that all properties carry similar risk. In practice, reserve needs can vary dramatically depending on the age, condition, and expected future expenditures of the property.

The Three Types of Reserves

Vacancy and Turnover Reserves

Tenants do not remain in a property forever, and eventually every rental property experiences turnover.

When that occurs, there may be a period without rental income while the property is being prepared for the next resident.

Depending on the condition of the property, turnover costs may include cleaning, paint, flooring replacement, appliance replacement, landscaping, and other improvements necessary to remain competitive in the market.

Owners should be prepared not only for the temporary loss of income but also for the costs associated with preparing the property for the next tenancy.

Maintenance Reserves

Maintenance reserves are intended to cover the routine repairs that occur during ownership.

Examples include:

Faucet repairs

Toilet repairs

Appliance repairs

Garbage disposal replacement

Minor plumbing repairs

Minor electrical repairs

These expenses are generally smaller than capital expenditures, but they occur regularly enough that every owner should expect them.

Capital Expenditure Reserves

Capital expenditures, often referred to as CapEx, are larger projects that occur less frequently but have a much greater financial impact.

Examples include:

Roof replacement

Furnace replacement

Air conditioning replacement

Water heater replacement

Exterior paint

Flooring replacement

Sewer replacement

Plumbing repipes

Unlike routine maintenance, these projects are often measured in thousands or tens of thousands of dollars.

Many of these expenses are not surprises. The exact timing may be uncertain, but owners generally know that these items will eventually require replacement.

Not All Properties Require The Same Reserves

One reason I moved beyond simple percentage-based reserve planning is that not all properties carry the same level of risk.

A newer home built within the last ten years has a very different risk profile than a property built in the 1960s. Even if both properties generate identical rental income, they may require dramatically different reserve targets.

The age of the property, condition of the major systems, expected turnover costs, and anticipated future capital expenditures all influence how much reserve capital an owner should maintain.

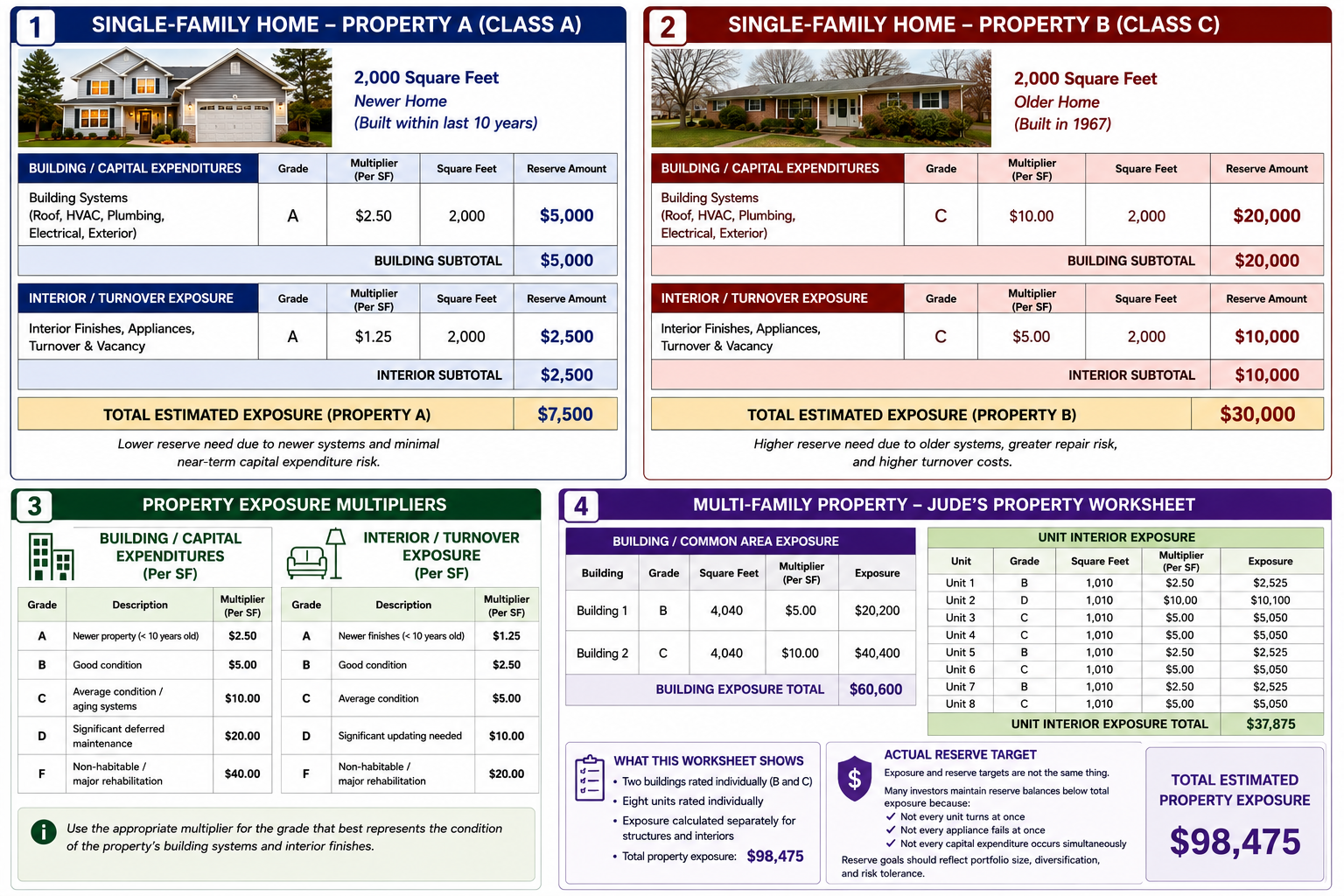

The infographic below illustrates how I think about reserve exposure.

The first example shows a newer Class A property with many years of useful life remaining in its major systems. While unexpected repairs can still occur, the overall exposure is generally lower because most major components are relatively new.

The second example shows an older Class C property. Although it may produce similar rental income, it carries greater exposure due to aging systems, future capital expenditures, and potentially higher turnover costs.

Neither property is necessarily a better investment. In many cases, the owner of the newer property paid more upfront for that reliability, while the owner of the older property accepted additional future repair and replacement risk in exchange for a lower acquisition cost.

The third section of the infographic contains the exposure multipliers I currently use when evaluating properties. The final section demonstrates how those multipliers can be applied to a multifamily property by evaluating both the buildings and the individual units.

The purpose of this exercise is not to predict future repairs with precision. Rather, it provides a structured way to evaluate relative risk and establish reserve targets that reflect the condition of the asset.

Exposure And Reserves Are Not The Same Thing

One of the most important distinctions for investors to understand is that exposure and reserve balances are not the same thing.

The multifamily property shown in the infographic has an estimated exposure of approximately $98,475.

That does not mean the owner should maintain $98,475 in a checking account.

The worksheet estimates the property's total exposure based on building condition, unit condition, expected turnover costs, and anticipated future capital expenditures. Reserve planning is a separate decision.

As portfolios grow, diversification begins working in the owner's favor. A tenant turnover in one unit does not mean every unit will turn over. Replacing a furnace this year does not mean every major system will fail this year. Likewise, capital expenditures rarely occur simultaneously across an entire portfolio.

For that reason, many experienced investors maintain reserve balances below their total theoretical exposure while still ensuring they have adequate liquidity to respond to expected events.

The worksheet helps identify risk. Reserve planning determines how much capital an owner chooses to maintain in response to that risk.

Where Should Reserve Funds Be Kept?

Every investor has a different approach.

Personally, I prefer maintaining reserves across several levels of accessibility.

A portion remains in cash for immediate needs.

A portion may be held in certificates of deposit or other conservative investments.

A portion may be invested in relatively stable investments that continue generating returns while remaining reasonably accessible.

For my own portfolio, I currently maintain approximately:

20% in cash

40% in CDs and similar conservative investments

40% in investments

The exact allocation is less important than ensuring the funds remain available when the property requires them.

Final Thoughts

Reserve planning is not about predicting the future. It is about recognizing that rental properties require periodic investment and preparing accordingly.

Every rental property will eventually experience turnover. Every major system will eventually reach the end of its useful life. At some point, every owner will be faced with repair, replacement, or renovation decisions.

Those expenses are not a sign that the investment has failed. They are a normal part of owning and operating rental housing.

The most successful investors I know treat reserve planning as part of the investment itself. They understand that cash flow and reserves work together. One generates returns today, while the other protects the property's ability to continue generating returns in the future.

A rental property should not be viewed as a paycheck. It should be viewed as a business, and every successful business plans for future expenses before they arrive.